Indian Markets: Sailing Through 2025's Correction Confidently

- IBS Times

- May 5, 2025

- 5 min read

By Ananya Sinha

In the ever-changing universe of finance, stock market corrections are a natural but disturbing phenomenon that puts investors' resilience and capital markets' strength to the test. At the core of this caution is the complex and frequently asymmetric interdependence between the Indian and US stock markets, augmented by the sudden emergence of retail investors, a majority of whom are unaccustomed to market turbulence. Since the Indian capital market is the epicenter of the country's growth narrative, it is important to identify the forces at work for investors, policymakers, as well as market participants.

The US Market: The Bellwether for Indian Equities

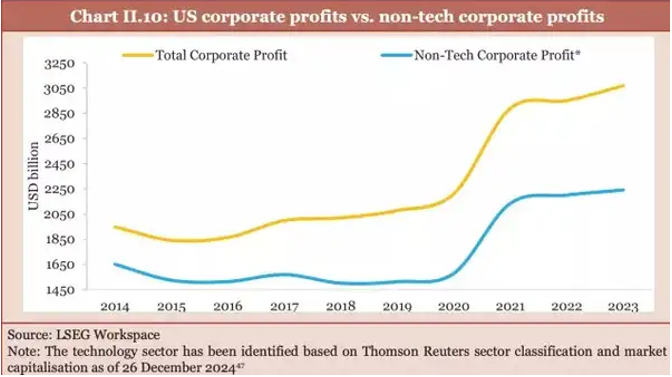

The US market, representing 75% of the MSCI World Index, is at record high valuations, the third highest ever on record with Shiller's S&P 500 CAPE ratio, an inflation-adjusted measure that smoothens out earnings to evaluate market valuation durability. A US market rally over the past few years has been highly concentrated among mega-cap tech companies like Apple, Microsoft, Amazon, Alphabet, and Nvidia. This focused leadership has driven valuations to high levels that are risky for a sudden correction.

Historical Correlation and Asymmetric Impact

From 2000 to 2024, evidence shows the Indian Nifty 50 index has returned negative in all but one of 22 occurrences when the US S&P 500 corrected by over 10%, averaging a fall of about 10.7%.

On the other hand, during 51 occasions of over 10% correction in the Nifty 50, the S&P 500 had positive returns in 13 instances. This reflects an asymmetric relationship in which US market fluctuations have a considerable impact on Indian equities, while Indian shocks hardly impact US markets.

In addition to this dynamic, US stock market movements "Granger-cause" Indian market returns, such that US market movements can forecast the Indian market's response to shocks, but not vice versa. This forward-looking relationship emphasizes the importance of Indian investors staying alert to US market movements.

Increase in Retail Investor Participation

A striking characteristic of the Indian capital market in recent years has been the dramatic rise in participation by retail investors. Investor numbers at the National Stock Exchange (NSE) reached over 10 crore during 2024, a three times rise in mere four years, and active traders during the cash market have grown from approximately 32 lakh in the early part of 2020 to 1.4 crore in November 2024.

This growth is fueled in part by young investors who came in post-pandemic, having experienced multiple years of bull markets without having to endure long corrections. Their inexperience in the market poses a risk, with a sudden correction possibly influencing market attitude and consumption, with spillover impacts on the overall economy.

Potential Cascading Effects on Capital Markets and the Economy.

1. Impact on Household Wealth and Consumption

Indian equity markets have become widely inclusive, with retail investors holding a large proportion of market capitalization. This broad-based ownership implies that a sharp drop in equity markets immediately impinges on household wealth.

This loss in wealth tends to find its way into less consumer confidence and consumption – a phenomenon referred to as the "wealth effect". As private consumption forms around 64.8% of India's nominal GDP in 2024, a fall in investor confidence tends to have a big impact on consumption demand, especially discretionary consumption of cars, electronics, property, and luxury items.

2. Impact on Corporate Margins and Industry Investment

Volatility in the stock market will typically reflect or cause changes in economic outlook and expectations of corporate earnings. Corrections can precede or signal earnings disappointments, which in turn feed back into business confidence and market sentiment.

Sectors with international exposure, like IT, pharma, and autos, are most vulnerable to external shocks in the form of weakening overseas demand and trade tensions, which can be more severe during market corrections.

3. Financial Sector Vulnerabilities

The banking and the non-banking finance company (NBFC) industry can get severely impacted in the time of stock market corrections. Rise in uncertainties and weakening of the economy have a tendency to drive up credit risks. Rising non-performing assets (NPAs) or bad loans may be the result of stressed borrowers, particularly as some segments and retail parts face financial pressures.

In addition, reduced market confidence can also constrict liquidity for non-bank financial institutions (NBFCs) and smaller lenders that rely on market funding. Strains in the banking sector spill over to broader credit availability, raising corporates' and households' cost of borrowing, which in turn may dampen economic activity further.

4. Systemic and Macroeconomic Risks

A market correction due to or coincidental with external shocks, such as rising interest rates, inflation, or geopolitical tensions, can amplify systemic financial dangers. India's strong integration with international capital markets makes it sensitive to shifts in US market valuations and monetary policy.

The capital markets of India have witnessed several long-term corrections with profound impacts:

1. 2008 Global Financial Crisis: The Indian market for equity fell by nearly 60%, dragged down by the US financial crisis. It took over two years to recover, showing the connected nature of the world and the drastic effect of the shock on capital markets.

2. 2020 COVID-19 Crash: Triggered by the global pandemic, the Sensex declined over 13% in a single day and declined by nearly 40% in weeks. The market recovered fiercely due to in-your-face interventions and retail participation.

3. 2015-2016 Chinese Market Volatility: A huge Indian market sell-off coincided with China's devaluation of the yuan and risk aversion worldwide, and this resulted in a prolonged correction period of over a year where investor sentiment was tested.

4. 1992 Harshad Mehta Scam: The market eroded almost 50% of its value over a long time after the scam, eroding investor confidence and prompting a regulatory overhaul in capital markets.

These incidents highlight how an external shock can combine with internal vulnerabilities to compound market stress, impacting the wider capital system.

Protective Measures and Investor Guidance

The Economic Survey and market experts advise investors to adopt a cautious, diversified portfolio approach in uncertain times. Strategies that are suggested include: Investing in large-cap, mid-cap, and small-cap stocks to offset growth and risk. Investing in financially healthy companies with healthy balance sheets and pricing power to weather storms.

Policy-level regulators continue to repeat investor education, transparency, and regulation, especially over speculative derivative trading, which has experienced a boom among newbie retail investors with high loss rates.

Conclusion

The Economic Survey 2024-25, alerting of a severe correction in the Indian stock market in 2025, is as much an advisory word as a call to preparedness. The Indian capital market, a vital channel for the creation of wealth and capital generation, is at a critical juncture driven by international variables, local investor groups, and economic fundamentals.Although the strong retail investor participation and structural changes have provided resilience, their linkage to an overvalued and sentiment US market brings risks that cannot be overlooked. Investors and policymakers need to navigate this space carefully, balancing faith.

Comments