Foreign Portfolio Investment in India: Trends, Risks, and Policy Impact

- IBS Times

- Jul 18, 2025

- 5 min read

By Sohum Shetty

Introduction: The Growing Role of FPIs

Foreign Portfolio Investment (FPI) refers to foreign investors—such as institutional funds, high‑net‑worth individuals, or sovereign wealth funds—buying financial assets in India’s equity and debt markets without seeking direct control. FPIs, previously classified under the Foreign Institutional Investor (FII) regime, are now governed by harmonized SEBI regulations introduced in 2014. Their participation has elevated India’s financial system’s depth, liquidity, and global integration. As a result, FPIs have become a barometer for global investor confidence and policy responsiveness in India.

Historical Trends: Upward Journey with Volatility

The Long-Term Uptrend

India's integration into global capital flows began in the late 1990s. Between 1993–94 and December 2011, cumulative FII/FPI investment rose from approximately US $1.6 billion to US $127.8 billion. By the mid‑2000s, portfolio liabilities—FPIs' cumulative ownership—accounted for around one-quarter of India's external liability position.

A Volatile Period (2024–25)

FPI flows in 2024–25 was marked by sharp swings. In 2024, net equity inflows were minimal at US $50 million, amid global rate hikes and cautious sentiment. Early 2025 saw outflows of over ₹1.5 lakh crore due to rupee depreciation and global uncertainty. However, sentiment rebounded by mid-2025, supported by the RBI’s 50-bps rate cut. May recorded ₹19,860 crore in equity inflows—the highest in the year—while late June added another ₹13,107 crore. Meanwhile, FPIs continued reducing exposure to debt, offloading ₹4,994 crore in June under the FAR route.

Early 2025 witnessed a mixed sentiment:

In February–March, FPIs withdrew over ₹1.5 lakh crore from equities, triggering rupee depreciation (~0.9 %)

Yet, toward late June, inflows rebounded: ₹13,107 crore over the week ending June 27 and May saw a monthly record of ₹19,860 crore

Meanwhile, modest outflows persisted in government securities—₹4,994 crore sold in June under FAR, compared with prior months’ larger exits.

Key Drivers Behind FPI Flows

Economic Fundamentals & Local Catalysts

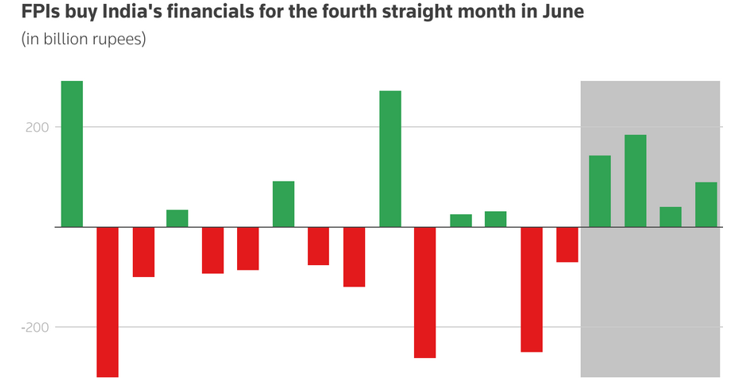

Monetary easing: RBI’s 50 bps rate cut and lower cash reserve ratios in May–June 2025 improved domestic yields, encouraging FPI inflows—₹145.9 billion into equities in June alone. Inflation moderation: Declining headline inflation has shored up market sentiment and attracted foreign participation in sectors like finance.

Sector preferences: Financials (~61% of June inflows), oil & gas (boosted by regional geopolitical easing), and cautious out-of-power and FMCG investments typify recent sector allocation trends.

Global Environment

U.S. rates and liquidity: FPI inflows are strongly moving in step with Fed policy. Low global rates drew capital to India in 2021–22 (₹2.74 lakh crore), while rising rates in 2024 prompted widespread withdrawals.

Geopolitical dynamics: Easing tensions in the Middle East led to improved energy sector sentiment; in contrast, global risk-off periods triggered FPI debt sell-offs.

Currency & Valuation Effects

Currency movements and valuation dynamics play a crucial role in shaping FPI flows. When the Indian rupee depreciates, it erodes foreign investors' returns in dollar terms, often prompting capital outflows. This sensitivity becomes more pronounced during periods of global monetary tightening, as investors shift funds toward higher-yielding or safer currencies. Furthermore, high equity valuations in India—especially relative to emerging market peers—can deter fresh foreign investments. These factors combined lead to greater volatility in capital markets, making exchange rate stability and valuation moderation important for sustaining long-term FPI interest.

Indian equity valuations: High PSG/earnings multiples have sparked concern among FPIs, leading some to pause new allocations.

Risks & Challenges Ahead

Volatility and Sudden Reversals: India’s FPI patterns are marked by sharp swings data underscore this: reversal from ₹8,749 crore equity outflow in early June to bullish ₹13,107 crore inflow three weeks later. Such volatility can strain markets and amplify systemic risk.

Currency Fluctuation Risk: Since INR weakness compounds foreign losses, it heightens investor sensitivity to global funding cost cycles and tightens FPI behaviour tied to currency views.

Overreliance on Foreign Liquidity: High dependency on FPI-driven liquidity exposes markets to risks from global shocks or policy missteps—especially in corporate debt, where stake concentration can amplify outflow impact.

Regulatory & Compliance Frictions: Participatory instruments like Participatory Notes raised transparency issues in the past. While SEBI tightened ODI rules in 2023–24, opaque structures remain a concern. Frequent shifts in norms (e.g., granular holding requirements, ODI curbs) can affect FPI flows and operational ease.

Policy Reforms: Enhancing FPI Engagement

Liberalizing Investment Caps

In 2025, the Reserve Bank of India (RBI) undertook a series of liberalization measures aimed at boosting foreign participation in the Indian debt market, particularly through changes in FPI investment norms. According to Reuters, one of the most notable reforms was the removal of the 30% cap on FPIs' investment in short-term corporate debt, a long-standing restriction that previously limited their participation in India's fixed-income markets. This move is aligned with India's broader objective of deepening its corporate bond market and making it more attractive for global investors. Additionally, the RBI scrapped the investment limit on a single corporate issuer for FPIs, allowing greater flexibility and portfolio diversification. These regulatory adjustments are expected to enhance India’s prospects for inclusion in major global bond indices and promote passive capital flows via global funds. However, while these liberalized norms improve market accessibility, analysts caution that the pace and volume of capital inflows will still be influenced by global interest rate trends and domestic currency stability. These measures aim to deepen liquidity, encourage diverse funding, and enhance market stability—but also require vigilance to prevent single‑participant dominance.

Stronger Transparency & Regulatory Framework

SEBI’s ODI rules: Expansion of granular holding disclosure and prohibition on certain hedging derivatives mitigate overleverage.

·KYC & operational simplicity: Streamlining through Category I FPI, Common Application Form (CAF) integration, and custodian oversight onboarding.

Policy Impact: Early Evidence

Debt Market Deepening: The removal of FPI investment caps in India’s debt markets is poised to significantly deepen both corporate and government bond segments. According to Kotak Securities, eliminating limits on one-year maturity bonds and concentration thresholds for corporate issuers expands the available pool for foreign investors. This move is expected to catalyse increased liquidity, drive down borrowing costs for issuers, and enhance the efficiency of price discovery. With fewer regulatory constraints, market participants can transact more freely, improving market depth and resilience. The measure aligns with broader efforts including anticipated inclusion in global bond indices—to attract passive and active foreign dollar flows, thereby strengthening India’s debt market infrastructure over time.

Equity Turnaround: In June 2025, FPIs resumed buying equities—₹145.9 billion in inflows, with financials and energy leading the charge. The rebound followed initial June outflows after the RBI rate cut, demonstrating policy-driven confidence.

Risk of Higher Concentration: Increased inflows into specific sectors highlight emerging concentration risk. Vigilance is required as FPI market influence grows.

Outlook & Strategic Implications

India as a Preferred Emerging Market: With global investors reassessing risk and seeking stable opportunities, India is increasingly being viewed as a favourable destination among emerging markets. Factors such as strong GDP growth, structural reforms, and regulatory liberalization—including relaxed FPI limits and anticipated inclusion in global bond indices—enhance India’s attractiveness. The RBI’s supportive monetary stance and macroeconomic stability further strengthen this positioning.

Need for Stronger Market Infrastructure: To capitalize on rising FPI interest, India must invest in strengthening its financial ecosystem. This includes improving market infrastructure, ensuring faster and more transparent settlement systems, and maintaining policy consistency. A robust regulatory environment, coupled with enhanced risk management frameworks, will be critical to managing volatility and sustaining long-term foreign capital flows.

Conclusion

Foreign Portfolio Investment plays a transformative role in India but also introduces cyclical vulnerabilities tied to global flows and currency dynamics. The last year’s data highlights this duality—periods of sharp outflows followed by record-setting inflows in May–June 2025.

Policy reforms—especially liberalized caps, regulatory transparency, and global index integration—are starting to shift market dynamics. The inclusion in bond benchmarks, coupled with eased debt thresholds, may usher long-term stability.

Nevertheless, to convert FPI into a sustainable foundation for financing growth, India must reinforce market infrastructure, macroprudential planning, and domestic liquidity buffers. If done well, India’s rising macroeconomic fundamentals, demographic strengths, and regulatory clarity could continue enticing foreign capital—while ensuring resilience against turbulence.

Comments