Value Investing in a High-Valuation Era: The Buffett Playbook

- IBS Times

- Mar 20

- 5 min read

By Vijay Venkatesh B

Warren Buffett bought his first stock on March 11, 1942. The Dow Jones Industrial Average was trading below 100 points. Today, it hovers around 43,000. Over eight decades, Buffett has watched markets swing from depression-era lows to post-pandemic highs, from dot-com euphoria to the 2008 financial crisis and back again. Yet his core philosophy has never flinched: find businesses with durable advantages, buy them at sensible prices, and hold them for a very long time.

Understanding the Core Principles of Value Investing

Most people reduce value investing to a single idea: buy cheap stocks. Buffett spent decades moving beyond that narrow definition. In his 2023 shareholder letter, he put it plainly: the goal at Berkshire is to own businesses that enjoy good economics that are fundamental and enduring. The word enduring matters. A temporarily cheap stock is not the same as a fundamentally sound business trading at a fair price.

This distinction traces back to the influence of Charlie Munger, whom Buffett described as the architect of today's Berkshire Hathaway in his 2023 letter, written after Munger's passing in November of that year. Munger pushed Buffett from the cigar-butt approach, buying dying businesses for one last puff of value, toward paying up for quality companies with genuine competitive advantages. The transition showed up in holdings like Coca-Cola, American Express, and more recently Apple, none of which would have qualified as statistically cheap at the time of purchase.

Quality, in Buffett's framework, rests on three pillars: honest and capable management, durable competitive advantages, and predictable long-term economics. When a business checks all three boxes, he is willing to hold it indefinitely. He has said Berkshire will maintain stakes in Coca-Cola and American Express for the rest of his lifetime, not because exit prices are unattractive, but because ownership of exceptional businesses compounds wealth in ways that trading in and out simply cannot.

Navigating High-Valuation Cycles: The Buffett Approach

Markets in 2024 and early 2025 have challenged investors across the board. Valuations by most measures, including the cyclically adjusted price-to-earnings ratio, sit well above historical averages. Growth stocks carry multiples that price in decades of future growth. In this environment, the temptation to either abandon equities or chase momentum is strong.

Buffett's response to this environment has been characteristic: patience backed by preparation. Berkshire's cash and Treasury bill position climbed to a record $334 billion by early 2025, a figure that drew considerable commentary from analysts who interpreted it as a bearish signal on stocks. Buffett corrected this reading directly in his 2025 shareholder letter, reminding investors that the great majority of Berkshire's assets remain in equities and that preference will not change.

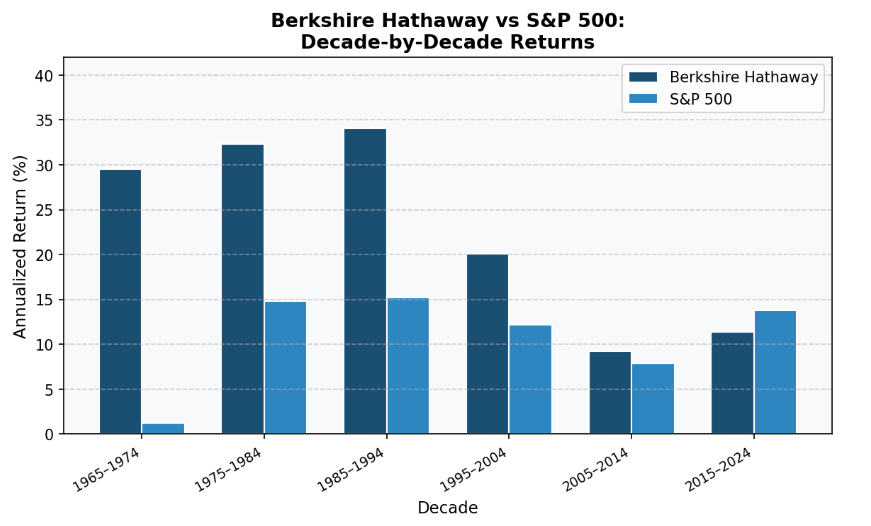

Figure 1: Berkshire Hathaway vs S&P 500 — Decade-by-Decade Annualized Returns (approximate, illustrative)

The cash pile, he explained, represents not pessimism but discipline. When very few things seem sensibly priced, holding cash costs relatively little in opportunity terms and preserves enormous flexibility for the moment when markets inevitably correct. As he noted in his section titled Our Not-So-Secret Weapon, dislocations and panics have historically been Berkshire's best buying windows, precisely because the company enters those moments with large sums and certainty of performance, two advantages most investors lack.

The Japanese trade conglomerate investments illustrate this patience in reverse. In 2019, Berkshire quietly built roughly nine percent stakes in five Japanese firms: Itochu, Marubeni, Mitsubishi, Mitsui, and Sumitomo. The logic was straightforward. Their stocks were trading at strikingly low prices relative to their financial records, their management teams followed shareholder-friendly policies, and the businesses generated dependable cash flows. In 2025, Buffett described the admiration Berkshire has developed for these companies as having grown consistently over the years.

The Portfolio: Where Conviction Meets Concentration

One aspect of Buffett's strategy that often surprises observers is its concentration. Despite managing an investment portfolio worth hundreds of billions of dollars, Berkshire tends to hold meaningful stakes in a small number of companies. The largest position, Apple, has at times represented more than forty percent of the publicly traded equity portfolio.

Figure 2: Approximate Berkshire Hathaway Portfolio Allocation (Based on 2024 13F Filing)

This concentration is intentional. Buffett argues that a business one truly understands and trusts is always preferable to diversification across businesses one does not. Diversification hedges ignorance, in his view, but it also dilutes conviction. For investors who have done the analytical work, concentration is a feature, not a risk.

That said, Buffett has trimmed Apple significantly since 2023, reducing Berkshire's stake by more than half through 2024. He offered no single explanation, though tax considerations and price appreciation were frequently cited. The move underscored another element of his discipline: no position is permanent if circumstances change, but sales should be thoughtful rather than reactive.

Decoding Market Signals: What Investors Should Watch

Running through recent letters is a consistent warning about the emotional character of modern markets. In the 2023 letter, Buffett wrote that although the stock market is considerably larger than in his early years, today's participants are neither more emotionally stable nor better educated than previous generations. Technology has made it faster to panic and easier to speculate, and the casino, as he put it, now resides in many homes.

This observation matters for practical investors because it identifies the structural advantage that disciplined, long-term holders possess. When markets seize up or irrationally reprice good businesses, the patient investor becomes the rational buyer. Buffett pointed to periods like September 2008 and the brief market closure of 1914 as examples of how quickly apparent certainty can dissolve, and how quickly it can return for those who have not sold in fear.

Applying Value Investing in Today’s Environment

Buffett’s Legacy Quantified

The Broader Market Outlook

Buffett's approach is not a formula that can be reduced to a checklist. It is a discipline built on decades of observing how businesses actually create and destroy value, how management teams behave under pressure, and how markets overshoot in both directions. The letters themselves are the curriculum: sixty years of clear-eyed analysis, honest accounting of mistakes, and unflinching belief in the compounding power of great businesses.

In expensive markets, his silence speaks as clearly as his purchases. The growing cash reserve at Berkshire does not mean stocks are finished. It means that right now, the right businesses at the right prices are scarce, and waiting is the disciplined response. As Buffett has written, doing nothing is sometimes the most powerful move an investor can make, particularly when the alternative risks permanent capital loss at too high a price.

For investors navigating 2025 and beyond, the shareholder letters remain the clearest roadmap available. They do not predict markets. They describe, year after year, how one investor has managed to compound wealth through every environment the last eight decades have produced. That record, 5,502,284 percent total gain versus 39,054 percent for the S&P 500 over the same period, speaks louder than any forecast.

Comments