Swiggy’s Mega QIP Draws Strong Subscription and Solid Pricing.

- IBS Times

- Dec 20, 2025

- 5 min read

By D Pavan

Swiggy Launches ₹10,000 Crore QIP to Strengthen Balance Sheet and Accelerate Growth Across Key Verticals. In a major move signalling its next phase of expansion, Swiggy has initiated a massive ₹10,000 crore Qualified Institutional Placement (QIP)—one of the largest equity raises in India’s consumer internet market this year. This fundraiser demonstrates the company’s commitment to strengthening its financial position and accelerating growth across its food delivery, quick-commerce, and emerging business verticals, particularly as competition intensifies in the hyperlocal delivery sector.

Swiggy’s shareholders overwhelmingly approved the QIP plan. At an extraordinary general meeting, 76.40% of shareholders participated, with 99.47% voting in favour. This strong endorsement underscores confidence in Swiggy’s long-term strategy and paves the way for its greatest capital-raising effort since the company’s IPO in November 2024.

What is a QIP?

When a company needs money to grow, whether it’s to expand operations, reduce debt, or invest in new opportunities, it has several options for raising funds. One of the quickest and most efficient methods for a listed company in India is something called a Qualified Institutional Placement, or QIP.

Think of a QIP as a private fundraising event, but instead of everyday retail investors, the company invites only large, experienced financial institutions such as mutual funds, insurance giants, pension funds, or foreign investors. These sophisticated buyers are known as Qualified Institutional Buyers (QIBs).

Because the participants are experts, the entire process becomes much faster, smoother, and more transparent. Companies don’t need to go through the long, expensive route of filing a detailed prospectus like they would for an IPO. Instead, they can raise large amounts of capital in a matter of days.

Floor Price, Structure, and What It Means for the Market?

Swiggy has set a floor price of ₹390.51 per share for the QIP, in accordance with SEBI’s pricing rules. Depending on investor appetite, the company may offer up to a 5% discount, which could influence final share allocation and the extent of equity dilution. At this floor price, Swiggy’s implied market capitalisation stands at around ₹97,400 crore.

The fundraising is expected to dilute Swiggy’s equity by approximately 9 to 10%, although the final figure may vary depending on the pricing. Investors responded positively to the announcement, with Swiggy’s stock climbing nearly 3% in early trading, an early sign of market confidence in the offering.

To ensure the QIP is handled with precision, Swiggy has appointed three leading financial institutions, Kotak Investment Banking, JP Morgan India, and Citigroup Global Markets India, to manage the process. The issue will be available only to Qualified Institutional Buyers, ensuring participation from experienced, long-term investors such as mutual funds, pension funds, foreign institutions, and insurance companies.

Why Swiggy Needs This Capital Now?

The timing of Swiggy’s QIP is no accident. The quick-commerce and food-delivery sector in India is undergoing one of its most competitive phases. Companies are racing to build capacity, expand into new cities, strengthen logistics, and offer faster deliveries. All of this requires substantial investment.

Swiggy’s rivals have been aggressively raising capital as well. Blinkit has secured ₹2,100 crore in 2025. Zepto recently raised $450 million both are rapidly expanding dark stores and pushing for market share.

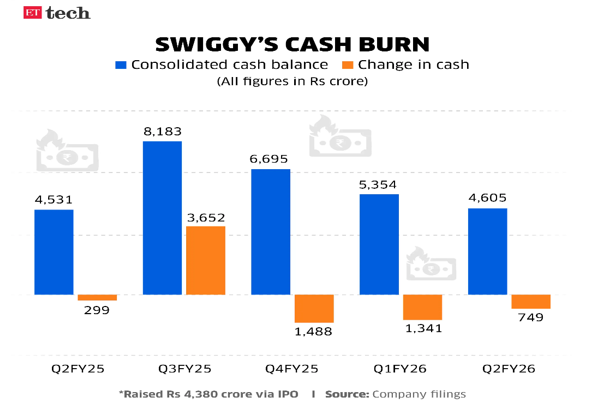

Swiggy’s own quick-commerce arm, Instamart, has been in a high-growth but high-burn cycle. The company recorded a cash burn of ₹740 crore in the September 2025 quarter, slightly more than Blinkit’s Eternal division, highlighting the intense capital requirements of the segment.

With competition intensifying and the cost of expansion rising, Swiggy’s QIP offers it the financial breathing room to strengthen its operations, invest in technology, support brand-building, and improve margins over time.

How Swiggy Plans to Use the ₹10,000 Crore

Swiggy’s preliminary placement document shares a detailed plan on how the company will deploy the new capital. The allocation reveals a clear focus on strengthening competitive advantages and boosting long-term capabilities.

Strengthening Quick Commerce – ₹4,475 crore

Nearly half of the QIP proceeds will be channelled into Instamart, Swiggy’s quick-commerce vertical. The investments will go toward setting up more dark stores and warehouses, enhancing inventory and supply-chain systems, improving last-mile logistics, and increasing Instamart’s national footprint. Instamart currently runs over 1,102 dark stores, and analysts say its Gross Order Value has grown more than 100% since the IPO momentum. Swiggy clearly wants to capitalise on.

Brand and Marketing Push – ₹2,340 crore

With competition growing, strengthening consumer recall is crucial. Swiggy plans to invest heavily in Marketing campaigns, Brand visibility, Customer acquisition, and Engagement programs. This sizable allocation highlights Swiggy’s intent to stay top-of-mind for consumers in a crowded market.

Upgrading Technology and Cloud Systems – ₹985 crore

Technology remains the backbone of Swiggy’s operations. The company plans to invest nearly ₹1,000 crore in Cloud infrastructure, AI and automation, Route optimisation, Personalisation engines, Fraud detection systems, and big data platforms. These investments will help Swiggy strengthen operational efficiency and enhance customer experience.

General Corporate Needs

Part of the capital will go into general corporate purposes, giving Swiggy flexibility to manage working capital, operational needs, and future investments. The company has committed to deploying the entire fund within three years, factoring in a 5% inflation rate for its capital planning.

Financial Performance: Strengths and Areas of Pressure

While Swiggy continues to deliver strong topline growth, profitability remains a work in progress. In Q2FY26, the company reported a Net loss of ₹1,092 crores. Revenue from operations is ₹5,561 crore (up 54% YoY),EBITDA loss is ₹789 crores.

The food delivery business, however, has been improving steadily. According to Nuvama Institutional Equities, Swiggy’s food delivery division has outpaced Zomato for four straight quarters it’s adjusted EBITDA improved from 0.2% in FY24 to +2% of Gross Order Value in FY25. Market share has stabilised, and margins have risen

On the quick-commerce side, Instamart is still behind Blinkit in profitability, valuation, and scale. Heavy investments, lower order values, and early-stage inefficiencies have added to its losses, estimated between ₹8,000 and ₹9,000 crore in adjusted EBITDA terms.

However, analysts believe Instamart has significant upside potential as Swiggy continues to add retail leadership, build scale, and optimise operations.

Boosting Liquidity Ahead of the QIP

Even before the QIP launch, Swiggy took steps to strengthen its cash reserves. In 2025, the company sold its 12% stake in Rapido, generating about ₹2,400 crore. This increased its total liquidity to over ₹7,000 crore, giving Swiggy a stronger financial position ahead of the QIP.

The divestment also helped Swiggy sharpen its focus on its core businesses—food delivery and Instamart—both of which sit at the heart of its long-term strategy.

Analyst Outlook: Optimistic Yet Watchful

Market analysts have generally reacted positively to Swiggy’s QIP. Nuvama Institutional Equities has initiated coverage with a ‘BUY’ rating and a target price of ₹510 per share based on a sum-of-the-parts valuation. The breakup includes ₹300/share for Food Delivery,₹144/share for Quick Commerce and additional value from other verticals, cash reserves

Nuvama expects Swiggy to close the profitability gap with Zomato by FY28, supported by scale benefits, better unit economics, and strategic investments.

Overview:

Swiggy’s ₹10,000-crore QIP is more than just a capital raise; it’s a strategic reset. It is a Turning Point for Swiggy’s Next Growth Phase. With clear investor support, a detailed deployment plan, and significant tailwinds in the digital commerce space, the company is gearing up for its biggest growth phase yet.

If Swiggy executes its strategy with discipline,balancing expansion with operational efficiency, it could strengthen its position as a leader in India’s food delivery and quick-commerce markets. The next three years will be crucial, determining whether this massive infusion becomes a turning point in Swiggy’s journey toward building a profitable and scalable hyperlocal services ecosystem.

Comments